And You'll Have Your Employer, Your Tenant & The Tax Mans Help To Pay It Off!

In 10 Years time, this $400,000 Property May Be Worth Around $600,000...

Isn't It Time You Found Out Why Having a Property In a Self Managed Super Fund is Possibly Australias Biggest Financial Secret?

Things You Should Know About Your

"Super Duper" Retirement

The Good News:

Recent Law changes enable SMSF to borrow to purchase a property. Why? Because the Australian population was fed up with losing money on the stock market...now, we have a choice.

In September 2007, the law changed to enable SMSFs to borrow money to purchase property... providing certain legal criteria is met.

Importantly, the legal criterion that enables a SMSF to borrow is not overly complicated and because the people at RM Group are recognised as the leaders in the industry, you could have your fund set up in no time at all. And the best part...they're in Newcastle!

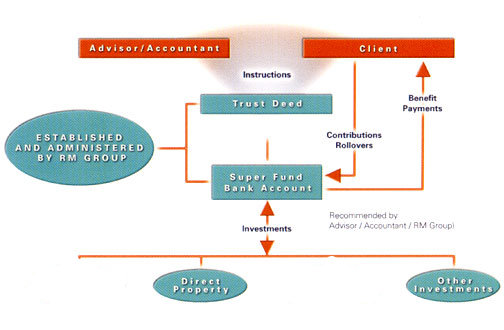

How Does It Work?:

The borrowed money is used to acquire an asset that is held in trust so that the Trustee of the SMSF (you) receives a beneficial interest and a right to acquire the legal ownership of the asset through the payment of instalments;

The Lender's recourse against the Trustee (you) in the event of default on the borrowing and related fees, or the exercise of rights by the fund Trustee, is limited to rights relating to the asset.

In other words, if the Trustee can show that the asset is one that the SMSF can own, the lenders only recourse against the Trustee for the loan will be the asset itself, and that through repayments to the Lender in instalments the Trustee receives a beneficial interest in the asset, the borrowing will be valid.

What Can't You Buy?

There are certain assets that a SMSF is prohibited from purchasing such as:

Property belonging to a member of the SMSF or a relative and;

In-house assets.

What's Involved in Purchasing Property Through a SMSF?

- Establish a SMSF.

- The SMSF chooses a Property to purchase.

- The SMSF establishes a Security Trust with a Security Trustee/s.

- Funds from the SMSF are used to purchase Property.

- If the SMSF does not have enough funds, the Security Trustee borrows money from Lender

(usually up to 70% of the purchase price).

- The Property is held by Security Trust for the SMSF.

- The Security Trust grants a Mortgage over the Property to the Lender.

- The SMSF collects rents, and makes Mortgage repayments to the Lender. Members of the

SMSF pay any shortfall from their contributions and if the contributions are not enough then

they will have to make extra contributions.

- When the Property is paid off completely it is transferred to the SMSF.

- Upon retirement the members can choose to sell the property or use it.

Can I lose money doing this?

Of course you can. If you bought the wrong property in the wrong place for too much money.

Really, if you wouldn't buy the house in the usual way with your normal income and borrowings,

you certainly wouldn't do it with your SMSF money.

The idea works, provided you buy an asset that has potential for both good income or rent and

good capital gain. If these two things happen, then your property is like a share and does all of

the things the Australian Taxation Office (ATO) wants to happen inside a SMSF.

"Want to Generate a Great Inheritance

for YOUR Children?

Property may be the answer..."

for YOUR Children?

Property may be the answer..."

Important information: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. For this reason, any individual should, before acting, consider the appropriateness of the information, having regard to the individuals objectives, financial situation and needs and, if necessary, seek appropriate professional advice.

You can find more info about the risks at www.asic.com.au

Have you lost BIG money out of your

Super Fund because of the repeated

Stock Market crashes?

Newcastle |